I’m happy to hear you are looking for a loan. Using other peoples’ money is a pillar of real estate investing. While not strictly required, it will get you head and shoulders above other people who paid cash for one deal instead of using that same money to get five deals.

It might seem easy. The bank knows what they are doing, right? If you think it’ll be just like getting a loan for your primary residence, then you are dead wrong. Go into the bank with this mentality and you are likely to get rejected. I’m going to assume you are ready to do this the right way – not just pretend you will be living in the house and lying to get a cheap loan. That’s a residential loan, and if you are thinking about using it to invest, don’t. Do this thing the right way.

How to Pitch Your Commercial Deal

Start with the mindset that you are selling something. The bank is your prospective buyer, and you want to sell them an income stream. That income stream has some basic parts:

- It will be a certain monthly amount (this is your monthly principal + interest payment)

- It will continue for a certain number of payments (this is your term)

- It will have a price (this is the principal)

The banker pays you the principal, which you pay to the seller of your deal, along with your down payment. You get the property, and the bank gets a promise that you’ll pay the monthly debt service for the term of the mortgage. The bank will evaluate this at the start – if it doesn’t work, you’ll get denied right away. But it doesn’t stop there, the underwriting still needs to happen.

Typically, your banker is the initial gatekeeper to the loan. They are like the bouncer at the bar. The bouncer can send you packing right away as they see fit, but get past the bouncer and you aren’t yet enjoying daiquiris. Sure, the bouncer has given you a pass, but the bartender still has to like the cut of your jib, and that’s the underwriting. Here’s how to impress your banker.

- Show confidence. You have to be excited about your own deal. If not, why should they be?

- Show that you know what you are talking about. Be prepared to use banker’s terms. I have a series on this you can read. Being knowledgeable about the lingo makes you look like you’ve done this before and gives you credibility.

- Give the banker top level details about the property. These details include the purchase price, the address, your intended improvements, and current tenants. If you’ve found any great ways to improve the place, such as adding a new unit or garage, explain that too.

- Make your ask. You need to come in to this meeting with what you want for amortization, LTV, rate, and term. I like to determine what I’d like them to be, then ask for a range that goes in my favor. For instance, if I want a rate of 5%, I’ll ask for a rate range of 4.5%-5%. This gives the banker options, even though they are only good options for you. Don’t go in with your hat in your hands asking for what they will offer – it won’t be great. This is a deal and requires negotiation and you have the benefit of making the first ‘offer’.

- If you will be shopping this deal around to multiple banks (not always a great idea) then let the banker know up front. And ask for the same terms at each bank.

Impress the banker, and you’ll move to the underwriter. The underwriter is the person(s) at the bank that looks at the details and makes a judgement about whether to offer the loan or not. If you’ve gotten this far, your banker likes the deal, and will act as your advocate with the underwriters. You won’t get to interact with them, so you need to impress your banker first. Since you won’t meet the underwriters, improve your chances with a smashing written presentation.

The presentation can be a slide deck or even a video, but I prefer a simple 6-page document made with Microsoft Publisher (they will need all the numbers anyway). It needs to be eye-catching but have the financial details needed to make it work.

The title page has a great picture of the property, the name of the deal, its address, and your contact info.

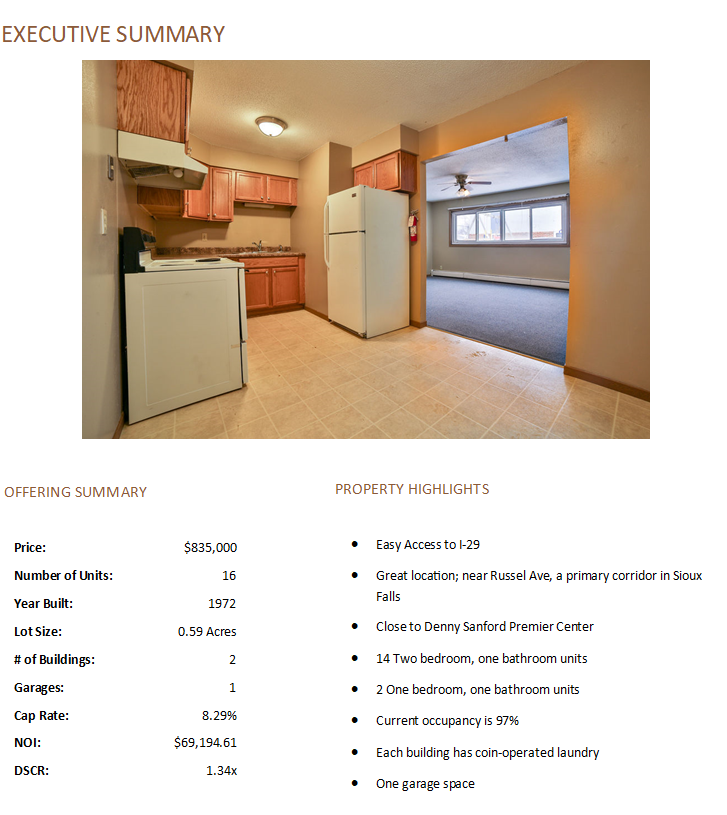

Next, you’ll write an executive summary. This is the place to put the top level information that you already gave to your banker. Also, add a few details that set this one apart.

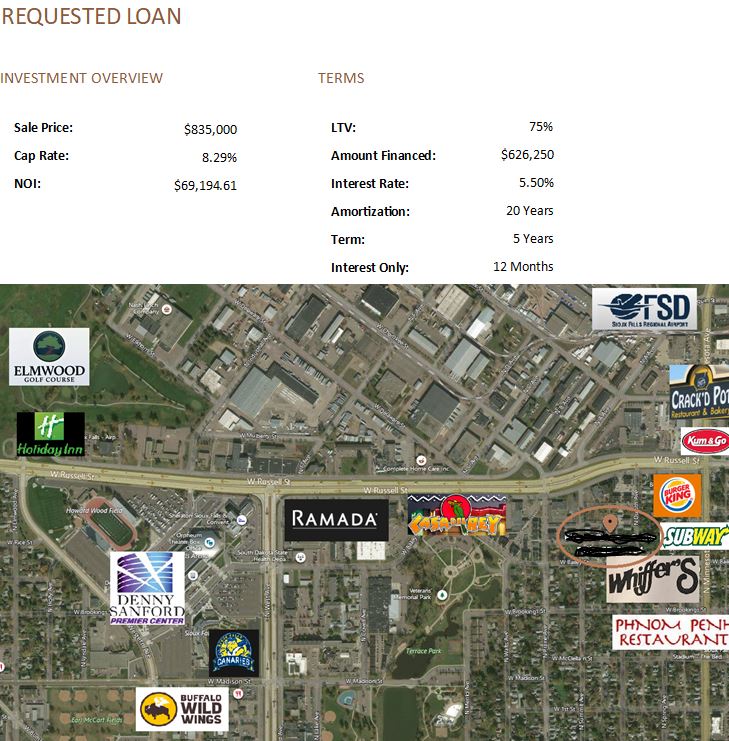

After that comes two pages of the financial details. You can grab it from your spreadsheet but you should make it look pretty – you are able to make a spreadsheet look pretty, believe me. The next page is the detail of what loan you requested.

Finally, you’ll have a page with some information on the assumptions you made, what you plan to do, usually increase the rents, and how to do it. Here is a great time to talk about your previous experience and why you are a great person to whom to offer a loan.Throughout this presentation you should have images of the property that you took when you did your walkthrough (after you asked for the seller’s permission, of course).

This document has to speak for itself. It needs to be simple and can be read in 5-10 minutes. You want to sell your deal, so make it pretty. Looking through this old one, I can see many areas I could improve. If you don’t want to do it yourself, there are some inexpensive creators over on Fiverr.com that can beautify your pages.

Remember, this is all about selling. You need to sell how great you will be and how great the deal is. Most investors waltz into the bank and ask for money. You are doing the same, except with a great presentation. Do this, and you’ll have a leg up on the competition.