So, you got your first loan on your investment property. You didn’t really think much about it. You assumed you’d have the same amount to pay over a long time and suddenly the loan would be paid back and you’d be happy. Well, it does work kind of like that, but it can get a lot more complex.

In school, you might have asked to borrow $5 from your friend Jimmy. He offered to loan you $5 and you would have to pay him back $1 every week for the next six weeks. Does that sound like a good deal? Depends on your situation.

You may be really desperate for the $5 so it might be worth it for you. For Jimmy, he is taking a risk that you will never pay him that $5 back. He is looking for enough upside (return) that he will bes willing to take the risk. Maybe he asks for some collateral, say that nice baseball card you own worth $10. Jimmy keeps that card. If you pay the entire loan, he gives you the card back. If you don’t pay, he keeps the card. Now, you are motivated to pay Jimmy back. This is a type of mortgage, or ‘dead pledge’. Either you pay in full, and the loan is dead, or you lose the card and it becomes dead to you. Don’t ask me – the French came up with it.

It’s easy to do the calculations when you are talking about round numbers, but what if you needed to borrow $6 for 45 days, how would that debt be structured? It would be helpful for Jimmy to have a rate of interest. Then he could just tell you he needs to have a certain percentage given back over a certain time period. Typically, the time period is annually, but it could be weekly or whatever else if Jimmy and you agreed.

If you are the recipient of the loan, you start by paying the interest as well as some part of your initial principal. On your $5 loan it would be 20% every week, for $1 due weekly. The complaint you might have is that once you’ve paid back the first dollar, you only have $4 in principal. If you owe 20% of that next week, you would only have to pay 80 cents. The next week, 64 cents. Going forward, you’d never get it paid off. Ideally, you want to have the convenience of paying the same amount each time with the guarantee of an interest rate and time period. You don’t want to get screwed out of a dollar every week if you have already paid back a bunch of the principal. For this, you’ll need to pay decreasing interest and increasing principal with each payment. This is an amortization, or ‘deadening’ of the loan.

The Deadening

Like going to the dentist, you want to deaden that loan the right way. This might be as fast as possible, but more likely, you want to know how much you pay every month. At the start of the loan, you are paying a lot of interest and at the end you are paying a lot of principal.

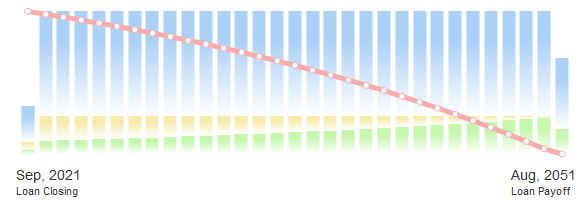

Have a look again at the image from the top:

Each multicolored bar represents one payment period. The yellow bar is your interest payment. It starts off high and decreases each time. The green bar is the principal payment. It starts off small then increases. Don’t worry about the blue bar, that is Amortization-calc showing you other bills such as tax and insurance. The height of the yellow plus the green bars remains the same. That is because your payment doesn’t change. The pink line is the total principal of the loan. It starts off going down slowly, and at the end goes down faster.

I use Amortization-calc.com. All you need to bring is a loan amount (this is the amount the bank brings, not the total price – you’ll have paid some of that off with your down payment), rate, and term (how long you will be paying). Check it out with some made-up data. I don’t think it’ll let you download to a spreadsheet. Excel has some formulas that can make the schedule for you, but they are a little complex unless you are an Excel wiz.

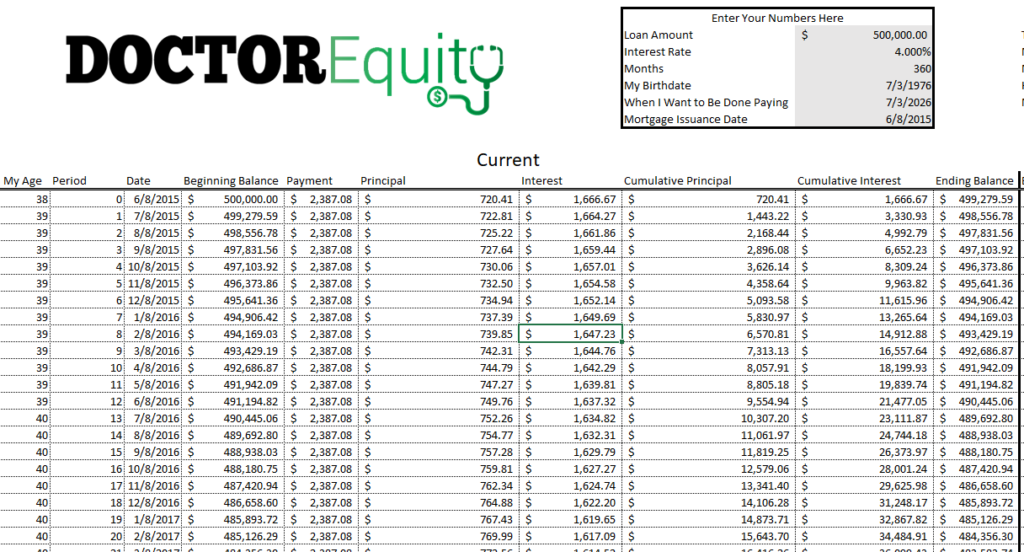

If you took each bar and put it on a spreadsheet you would have an amortization schedule.

Why Do I Need The Amortization Schedule?

The schedule is intimidating, but it is helpful because at a glance you can find out how much you’ll pay monthly. Also, you can find when you will have the loan fully amortized (paid off). You can find out how much principal and interest you are paying each pay period.

Another important reason to keep this handy is that your bank might request it in a Debt Schedule, the document that shows how much you owe on loans and when they are paid off.

When you are evaluating a property, you’ll need to know how much you’ll pay in the loan. This payback is an important expense. The amortization schedule can tell you very quickly. Use the schedule next time you are evaluating a deal.