The Capitalization Rate (Cap Rate) is another way to look at the return an investor gets on his or her money. Last time we saw a negative impact of using the bank’s money. In reality, you will sometimes find terms with the bank that work for your deal; sometimes not. Each deal can be wildly different because of the financing used. Wouldn’t it be nice if there was a way to remove this from the equation?

The Cap Rate is a way of evaluating a deal that removes any adjustment for debt service. It looks at the purchase price of the deal, not what you put into it. It doesn’t care how much money you have in the deal.

Let’s say you purchase your $100,000 in gold bullion as before. You get 1% return on your investment as before, and, after a year, come home with $101,000. It cost you $600 in security system payments.

The Cap Rate is the ratio of profit divided by the price paid to purchase the asset. Because it is a ratio, there is no time-frame associated with it, but we usually do the calculations over a year, same as with the Cash-on-Cash Return.

($1000 – $600) / $100,000 = 0.4%

What if we get the bank to finance $75,000? Then the equation is

($1000 – $600) / $100,000 = 0.4%

Does that look familiar? It looks just like the Cash-on-Cash Return. And it is. It is exactly the same thing for all deals where you use your own money and don’t do any financing. The Cash-on-Cash return gives us a better picture of our individual deal when we are using financing (bank or other lender) but makes it difficult to compare deals with one another. For that, we forget about the financing (temporarily), and use the Cap Rate

The Cap Rate doesn’t care about your financing. Recall the Cash-on-Cash Return here was

($1,000 – $600 – $500 * 12) / $100,000 = -6.5%

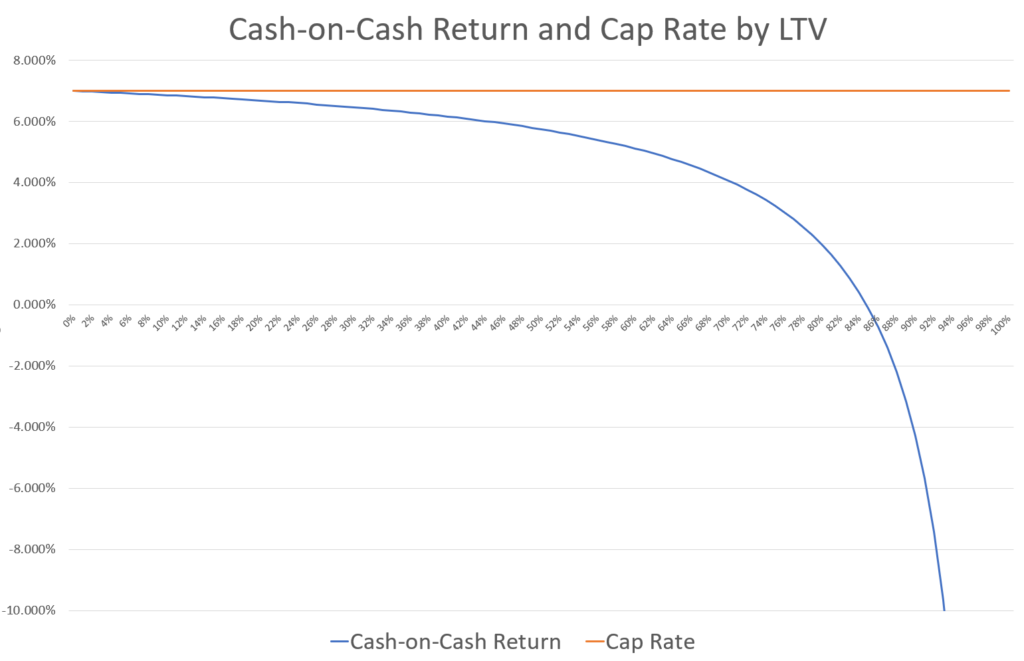

As you put more money into your deal and have less financing, the Cash-on-Cash Return trends toward the Cap Rate and once you have no financing at all, they are equal. Here’s a handy graph to help picture this:

estimated yearly profit $7,000

I use a spreadsheet and plug in the terms to get this graph. You can see that when the LTV is 0% Cash-on-Cash Return equals the Cap Rate. As you finance more and more of the deal, your margin gets less and less and it really starts going down after about 75% (sorry it is hard to see on my image above). When you look at a deal, it is helpful to generate a graphic like this to see what range of LTV you can accept. I’ll give my spreadsheet to DoctorEquity members.

Let’s say I purchase a rental property for a certain price, we will call it my investment. I collect rent on this property for a year. Sometimes the property is vacant but mostly there is a tenant paying and I keep a record of all the rent income I get. I also have expenses like property tax and I happen to remove snow in the winters. I also have a monthly insurance payment. I add up all of these expenses except debt service at the end of the year. When I subtract my expenses from my income, I get a number that you might call profit. The cap rate is the yearly profit I get per dollar of my investment. We represent it as a percentage rather than a number.

The Cap Rate tells me how much money I expect to receive in profit over a year for a given investment amount. For you math-heads the equation is as follows

Cap Rate = Profit / Investment

But there is one catch. The Cap Rate doesn’t take into account debt service. Debt service is the amount of money you pay to the bank over the year.

Why doesn’t the cap rate use debt service?

It’s a difficult question to wrap your head around when you are starting out. The reason is that we are looking for that apples-to-apples comparison. You will hopefully be negotiating with the bank(s) to find the best terms for a mortgage, or better yet, you will pay cash and avoid using the bank. If the bank did finance the deal, it would lend you a percentage of the purchase price, and you would have to come up with the rest, a Down Payment.

Another bank might be willing to give you a slightly lower interest rate, but a shorter term. It might give you a non-recourse loan (if your business defaults, the bank can take the property but can’t collect the debt from you personally). There are many other variables that could enter the equation. The next person who was evaluating the property might be able to get a vastly different set of terms from their bank. If we factored debt service into our cap rate, then the Cap Rate would be wildly different for different deals and buyers and we wouldn’t be able to compare them.

Also, you will be evaluating many deals well before you are talking to the bank. you wouldn’t want to waste the banker’s time on every deal you look at because most deals you won’t take. Because of this, you won’t be able to get the bank’s terms until later, anyway.

The Cap Rate is good to compare across multiple deals. Some people set a line and will only look at deals with a certain Cap Rate or higher. The Cash-on-Cash Return is a more personal way to evaluate the individual deal. Some people set a line and reject deals that fall below it, but I don’t recommend comparing Cash-on-Cash Return across multiple deals.

But maybe you are just starting out and want to evaluate a SFR property. For that, we use some other rules.

Let’s talk about that next week.