Rules. Rules. Rules. It’s easy to get them mixed up. That’s why I’m here to help.

Last time, we looked at my first rental through the lens of someone trying to make a profit on a quick sale (a flip). You could look at your properties that way, but do you really want to be a flipper? The problem is, these properties (hopefully) make you a profit. You will then have to pay tax on the profit as it becomes part of your general income.

You, however, are a high-income earner. You don’t need more income and you certainly don’t need another job. Flipping is hard work and I look it as a job more than an investment. A flipper is in the sales business, buying something for a price and selling it at a different price. The difference is his profit. You are an investor: you put your money into a venture and profit from the income the investment produces continually.

An Investor is willing to put money into something and plans on a long-term gain. For you, it will be monthly rent payments that will go in perpetuity. If you don’t make a profit immediately (as a flipper would hope to) you don’t care. In fact, you would rather said profits were somehow put back into the business to avoid being taxed. You have the long-term horizon for which to plan. You need a different rule.

The 50% Rule

The 50% Rule assumes that expenses on a small rental such as a SFR should take about half the income of the rental. For instance, if the rent is $1,000, the expenses should be $500. It’s that simple. Remember that expenses are all the things you have to pay for as the owner, except your debt service. One thing you will note is that while expenses take half of your profit, leaving half left for you, your debt service better not be more than the remaining 50% or you’re under water.

What about Dumpy?

You remember Dumpy? My first rental? OK. Let’s look at Dumpy with the 50% rule: To do this, you need to have a good estimation of the rent your property will get. This is critically important, like the blood pressure in a trauma patient. Don’t forget about it.

How do I figure out the rent?

The first step is to know your area. You will be able to get a feel for the rent after doing this for a couple years, but each area is different. One town ten miles away can have rents much higher than the other. When starting you might ask your real estate agent. You need to be very, very careful here because many agents think they know about rentals but don’t. By now you should be in an investor group. They will have some ideas for you. Another way will be to grab the rental magazines at the front of the grocery store. I know you usually ignore these, but renters don’t. Just check. They’ll be there. Finally, check Apartments.com and Craigslist.com. But, keep in mind, these rents are for those that haven’t been rented yet, otherwise they wouldn’t be advertising. The rent might be too high.

For Dumpy I threw out $1,100 a month after talking to my agent at the time. I realize now this was too low. That place should have been getting $1,300. If I would have done it right, I would have calculated a 50% rule of $650. This is the estimated monthly expenses for Dumpy. An astute reader will notice that the estimated expenses will rise with the rent, and that is absolutely right. The estimated expenses. If you can get more rent, the rule estimates higher, but as the rent goes up, your expenses don’t always rise. Just as our other rules have flaws, this is a flaw with the 50% rule. You need to accurately estimate the rent for this. In my estimation, it overestimates expenses, but that is good. The overestimation is a buffer for you and it translates into profit.

Because Dumpy is a SFR, the tenants are responsible for paying for water/sewer, electrical, gas, snow removal, and lawn care (usually the case, but not always). The owner pays for repairs, taxes, and property insurance. Dumpy’s monthly figures look like this:

- Repairs $130

- Taxes $246.85

- Insurance $133.33

- Total: $510.18

This is less than the $650 estimated by the 50% rule, so this rule would tell us to go ahead and buy the property. How did we get repairs? In larger properties we divide repairs up into repairs and capital expenditures. I’ll explain these later. I estimate repairs for SFRs at 10% of the rent. Higher rents usually mean that the tenant gives more repair calls so I think 10% is a good rule of thumb. In practice, you will have some months with repair bills that are very large and most months will have no repairs; this averages it out monthly.

I thought you were going to tell me how much to pay for the property!

It is actually buried in there – remember I said that the other 50% is the income and your debt service must not be greater than that? Whatever you pay for the place, your monthly bank payment needs to be lower than the money left over after expenses. Work backwards from this on your deal to find out how much you can pay.

Dumpy’s mortgage had a monthly payment of $1100, which means I really botched this one. In a previous post I told you I was (and still am) willing to subsidize this with my considerable income to get it paid off quickly. That strategy is not sound for everyone, particularly those with low income or those who want to maximize their leverage when investing.

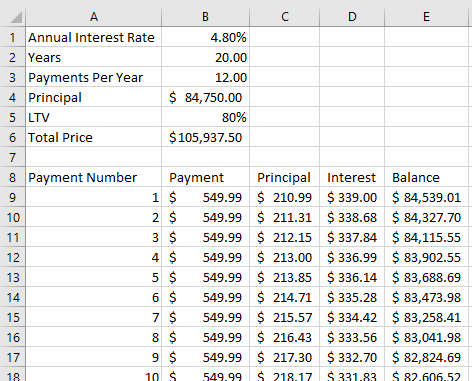

If I had used the 50% rule based on what I thought the rent would be, $1100, I would have calculated $550 per month for expenses. I would then have $550 left over for debt service. Working backward, I need to know what my interest rate and term will be: just talk to the bank. For me, it would have been 80% LTV at 4.8% over 20 years for a typical mortgage. Please recall from a prior post that I did my loan differently to pay it off fast.

With these figures, I can just plug them into my amortization spreadsheet (sign up for our email list and I’ll send you a copy)

I just keep changing the principal until the payment gets to about $550.00. This tells me that the most I can borrow is $85,750.00, and with my down payment, the most I can pay is $105,937.50. Not far off!

The 50% rule is best used to estimate your expenses from the rent you will get. There are many flaws to this, not least of which is a dependence on an accurate rent estimation. Also, if we actually did pay what we estimated, there would be no extra income for emergencies.

Isn’t there a better way to decide how much to pay?

That all depends. Just remember that You are the only one who can decide this. You need as much information as you can get to make an informed decision. But, since you asked, if you want a way to estimate how much to pay for the place you need another percent rule: the 2% Rule.

See you soon.