We are already half-way through the year. The rest of the year brings uncertainty. There’s a lot of money waiting on the sidelines right now, despite the inflation of the past 2 years. We were up to mid 8%s and everyone was complaining about how high their eggs cost. Now, eggs are still expensive, but people are getting used to it and the inflation rate is down to a reasonable 2.97%. You can credit the Federal Reserve for a large part of this. You can also credit the Fed for the high interest rates you are staring at from your bank.

We are now at a similar rate we saw before the crash of 2008. This is making some people nervous about a possible crash of some sort. “The Fed has to start lowering rates soon,” they say. They are wrong.

Will Rates Go Down?

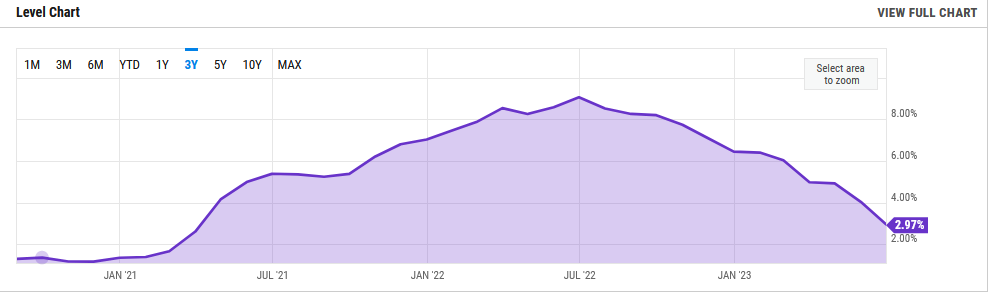

Here’s our inflation rate over the past 3 years.

It’s done exactly what the Fed wanted – go down to around 3%, a rate that they like. Unemployment rate is still low at 3.5%. All these primary metrics are what the Fed wants. They have no incentive to lower that rate right now. People are working, they are able to spend money and keep the economy going, they are not seeing any pain in the housing market – though investors might be.

Amazing Prediction 1: Interest rates will not go down for 6 months. That’s based on a prediction that unemployment and inflation stays the same. I think they will.

Will Rates Go Up?

That one is a little harder. There is still some room to go lower on inflation, but the Fed is probably hosting a party right now in some government basement with government cheese and imitation crab dip about how successful they have been. They won’t want to upset the apple cart.

Amazing Prediction 2: We see another 0.25 point increase in the federal funds rate – which feeds into what you pay at the bank – over the next 6 months. That’s it. They need to keep up the tough guy unpredictable look and are going for perfection.

So, What Do I Do About It?

As I’ve said recently, the unemployment rate is going to be the bellwether of what our rates will do. If that starts to tick up, the Fed will start to give us some interest rate relief. Until then, you need to watch for owners who have a significant life event, like losing their job, or getting divorced. They will need to move out of a low interest rate property fast. These are the ones who will have clear eyes about how much a buyer can pay with respect to the current rates. Start talking to your banker(s) now.