Welcome back to the Multifamily Underwriting Series. This is number 8, The Metrics. Here are the previous posts in this series:

- Introduction

- Initial Evaluation

- Secondary Evaluation

- Gather Information

- Analyze Income

- Analyze Expenses

- Financing

If you haven’t gotten caught up, I suggest you do so before reading this post. For the rest of you, let’s talk about the numbers. Yea!

Wow, this series has gotten quite long. It’s wild how many details go into underwriting a deal. It’s all in an effort to first, keep you from losing money, and second, to make you and your partners some money. Well, hopefully a lot of money. I certainly can’t guarantee that you will, but this is all about minimizing the risk and maximizing the gain. Don’t be afraid to dump a bad deal, even if you’ve spent hours on it. Conversely, don’t be afraid to strike on a good deal once you’ve done the underwriting. Good deals don’t come along often.

The Metrics

Sorry for the excessive use of business-speak with the metrics and this one: Let’s drill down into the details. I really hate that one. Sorry.

If you have your spreadsheet set up correctly, you should have everything populated by now. This step is all about the calculations, which it should do for you. I’ve colored the cells in a gray to tell myself not to change anything in them. I haven’t locked them because from time to time I do make changes during the stress testing (which will be in a future post).

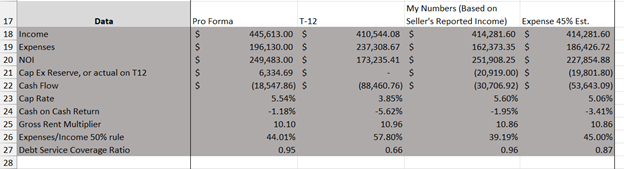

Hopefully you’ll remember from last time about our 47-unit deal. We had some warning signs in the expenses section, but not enough to dump the deal. We have 4 columns, the Pro Forma, which are the seller’s wishful numbers, the T-12 which are the seller’s reported actual profit and loss, My Numbers (really Your numbers) which are my realistic expectations, and Expense Ratio (here, 45%) which is an estimation based on past investment experience. Each one shows a different picture. None of them are perfectly correct. Let’s go by columns.

Pro Forma

Here, we have income, expenses, and NOI. These are ordinary income, from which is subtracted ordinary expenses, to arrive at the Net Operating Income. On row 21, we have the capital expenditure reserve. This is the amount of money we are saving each year for that inevitable large repair or upgrade. An example is a replacement roof. It’s not if, but when, and you must be saving this. But, it’s not an ordinary expense, so it comes out after the NOI. Which means it won’t affect the cap rate or the value of the property. Here’s an example of this in action:

The property has all old roofing. There are multiple buildings in our example, but I’m going to refer to it as one roof for clarity. And because I’m too lazy to find out if the plural is ‘roofs’ or ‘rooves’. There are no leaks found on inspection, so you could start renting it out as-is, but you expect it will need replacement in the next few years. You contact 3 roofers and you estimate that it will cost $100,000 to redo the roof. You ask the seller to give you a 100k credit. The seller says, “But the roof is working fine right now.” Clearly there is some credit that should go based on the life of the roof, so you settle on 60k (or whatever). You’ll enter this roof credit in the spreadsheet as a decrease in offer price (see previous posts) rather than an expense, because it is not recurring and not an ordinary expense. In the future, you’ll have to still come up with the 100k cash for the new roof, so you better start saving now. In this example, you might expect to replace the roof in 5 years, so you’d need to save 20k per year in line 21 to be ready. But in this example the 47-unit the roof is nice, so we won’t be doing that. Make sense?

Cash flow is on line 22 and is what is left of the NOI after we take out our mortgage and cap ex reserve. In the pro forma, at -18k it’s ugly and is a huge red flag. Even the seller’s rosy numbers cause a loss. If the cash flow is negative, this is a very bad sign, but don’t dump the deal yet. There’s still a chance and I’ll explain in a bit.

Now, the spreadsheet gives us the metrics we have been looking for. I’ve got them in order on rows 23 to 27. Notice how the cap rate is 5.54%? Sellers will love to talk this number up on their promotional materials, hoping you’ll ignore the cap ex need and financing. Don’t fall for it. Even that cap rate is low, but in some markets and times, that would be good. Cash on Cash return is next and it is dependent on the cash flow. When it is negative, the deal loses money and is another red flag related to cash flow.

Next, we have the gross rent multiplier, or GRM. This is the number of years of rental income it would take to pay back a 0% loan on the property. Or, it is the number of years of rental income it takes to equal the purchase price. On Class A units, our 10.10 is pretty decent. As we go to Class B and C, we want the GRM to be lower, maybe 4-8, depending on how nice a property it is. Use those numbers only for rough reference, the GRM is a poor predictor of quality of investment. In reality, it’ll take you a lot longer to pay the property off because you have something everyone has and the GRM ignores: Expenses.

Line 26 is the Expense Ratio. I like it to be lower than 50%, but this also is just one of many metrics and should not be used alone. We talked about the expense ratio in a previous post in this series.

The Debt Service Coverage Ratio (DSCR) is a very important metric for your bank and I put it in here so I can communicate with my banker about this. Briefly, the DSCR is ratio of NOI to the yearly debt service (principal and interest). The bank wants your project to comfortably be bringing in money, so wants a higher DSCR when possible. The DSCR requirements vary by bank but many want it to be at least 1.2 in my experience.

T-12

This one is similar to the Pro Forma and again, all the calculations are done for you. Of note, you may have to write in something on the cap ex, line 21, if the seller reports it. More often than not, they report nothing and you have a 0 here. It’s very helpful to see how they are doing and it looks bad. The thing is, their numbers are based on what they paid for the place when they bought it, so in the end, not terrible for them. If they reported their debt service to you, you could put it in line 54 (see last week’s post), but then you’d also want to know what they paid for the place. That could be found by checking county records, or from your real estate agent if you wanted it. I don’t really care how they are doing, but want to see what would happen if I bought it today and did just as well as they did, so I keep the purchase price and financing to what I will get. With that, we get these nasty numbers.

My Numbers

Generally, these numbers should be better than the T-12 but not as good as the Pro Forma. These are the numbers you predict you will get. You’ll probably be putting money into renovation (which you’ll need to take off the top offer price usually) and raising the rents. Hopefully, you will also improve expenses, but all of these things take time. If you want to know how I calculate income and expenses, go back to those posts. Notice that line 26, Expenses/Income is 39%. This is a red flag for me that I’ve mentioned in a previous post. I’m probably mis-estimating expenses. Nonetheless, the cash on cash return is negative here too. Another red flag.

Expense 45% Est.

This is based on the expense ratio I have set for my project. Not much more to comment on this one.

Overall

Overall, the DCSR is very low. I don’t know of a bank that will finance this deal. The cash on cash return is negative. I don’t know of an investor worth his salt who would purchase this deal. But all is not lost, we can now look at the numbers in more detail and arrive on a price we need to purchase the property. Since we are already under contract, this will often come into play as a credit the seller will give to us.

A note: At this phase, buyers will often ask for a huge credit for no reason to try to get a great deal from the seller. This is called retrading and you shouldn’t do it. It relies on hoping the seller is desperate to complete the deal which is nearly across the finish line and will take a haircut to do it. That’s a terrible way to do business and will give you a bad reputation. Only ask for what your numbers find and be ready to back the ask up with actual findings from your due diligence.

I want to caution you that even these metrics (if great) alone are not enough to give a thumbs-up to the deal. Everything we talked about in the last 7 posts have to be positive to even consider going this far. If the metrics work out, you still don’t have yourself a deal. If they don’t work out, you might still have a deal with a reduced price or credit, which is why we need to go on to next week’s post – stress testing.