Welcome back to the Multifamily Underwriting Series. This is number 7, Financing. Here are the previous posts in this series:

- Introduction

- Initial Evaluation

- Secondary Evaluation

- Gather Information

- Analyze Income

- Analyze Expenses

If you haven’t gotten caught up, I suggest you do so before reading this post. For the rest of you, let’s talk about your bank.

The Bank

If you’ve been following my instructions, you have already talked to your commercial banker and gotten a ballpark rate and terms. Remember that these are negotiable, but you at least have a starting point. That information helped you in your search for properties. Now you’ve found one and are doing the underwriting.

Now, it’s time to put in the financing information into your underwriting spreadsheet.

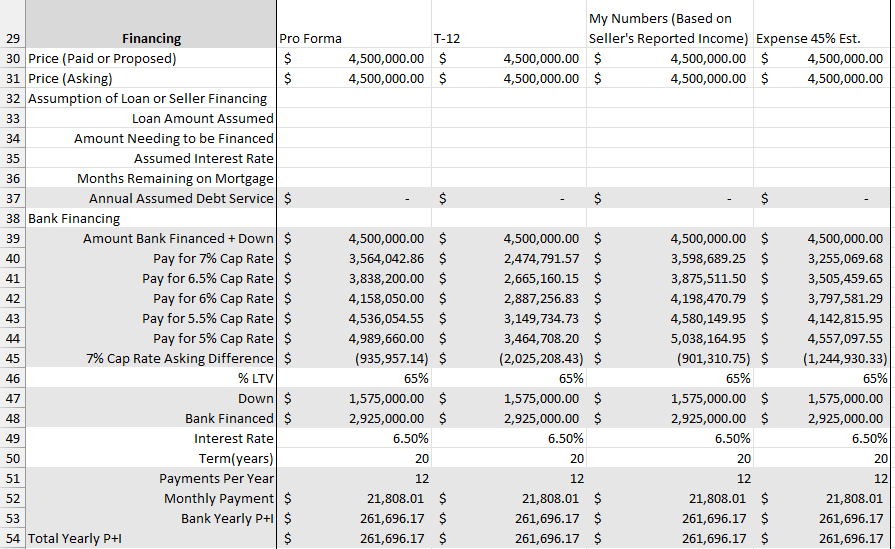

This part’ll take a little explanation. Line 30 and 31 are the price. Asking price is what you heard the seller wants. They’ll often accept less, so, line 30 is the one that all the spreadsheet math is working on. You’ll change that number to help in your deliberations, while the asking price stays the same and is a reminder of how far off their price is from the ‘true’ value that you will calculate.

Lines 32-36 are if seller financing is involved. For this example, there is no seller financing, so these are left blank.

The lines you’ll need to edit are colored white. The calculated ones are gray. Line 46 is the Loan to Value, or how much the bank will finance of the purchase price. The rest is the down payment. You can often get an LTV of 75% or 80%, though. 65% is a more conservative bank, which I’m seeing right now. The spreadsheet will calculate the down payment and the bank financed amount in lines 47 and 48. You’ll need to place your quoted rate and mortgage term next. With this information, the spreadsheet will calculate your monthly and annual payment (principal and interest). The last line, 54, totals both the bank financed payments and seller financed payments, if any.

Lines 39 through 45 are some helpful calculations to show you the value at certain cap rate detents. It is using numbers that we haven’t talked about yet, namely the NOI. We will get to that in the next post on metrics. It’s basically saying that based on the numbers of the column (pro forma, T-12, My Numbers, etc.) you’d have to pay x amount to have a 7% cap rate deal. Line 45 is the difference between the paid price and a 7% cap rate, what I typically shoot for. Looks like the pro forma is off by 935k! That doesn’t mean the deal is dead, but it’s a giant red flag.

See you next time for the fun part, the metrics.