Welcome back to the Multifamily Underwriting Series. This is number 6, Analyze Expenses. Here are the previous posts in this series:

If you haven’t gotten caught up, I suggest you do so before reading this one.

Our 47 Unit Example

You’ll remember that we went through all the income last time. We had to make some assumptions about the rent we think we will get. We took the seller’s word for some other sources of income. We had to make a gut decision on whether we would get this same income or not.

We will be doing a lot of the same calculus today, but with expenses. Unfortunately, expenses is the #1 area where sellers can massage the data in their favor. You have to keep an eye on what expenses you will have as well as what they report.

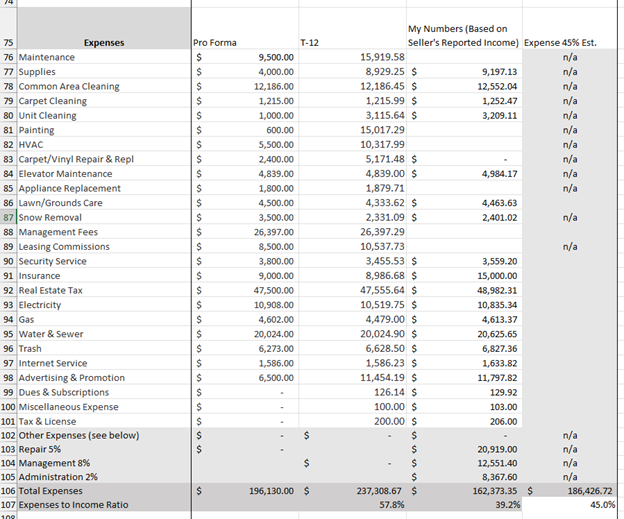

In the T-12, the seller will usually have a line-item list of expenses. They usually will have large and small ticket items like property tax and miscellaneous expenses. If you are lucky, they use QuickBooks and will give you a spreadsheet from that program. Take all their expenses and copy them into your spreadsheet. It’s a lot easier if you mirror their items rather than using your own list. Then, estimate what you’ll have to spend in My Numbers. When you are done, it’ll look something like this:

Again, look at the difference between the T-12 and the Pro Forma. There’s a 40k difference! With this spreadsheet you can scan down and see a few estimations they have made. Pro tip: be wary of round numbers, such as Supplies. These are likely just a guess. The major discrepancies are Maintenance, Supplies, Painting, HVAC, and Advertising. You will need to question why they estimate a new buyer can do so much better.

For my numbers, maintenance is included in repair. For a new-ish property, I estimate 5% of the gross scheduled rent, which you see in line 103. I don’t know what they have for supplies. I put that in with maintenance but they had $9k and I don’t think I’ll do much better until I ask what this was for. Painting, HVAC, Appliance replacement are all capital expenditures (things that are not annually recurring and improve the rent). These should show up later and don’t belong in expenses. You’ll see they realized this to an extent in the Pro Forma line 81, where painting goes down to $600. Line 91, Insurance, seems very low for a 47-unit property. Sellers often are underinsured. You shouldn’t be. Management and Leasing Commission are rolled into one for me and are in line 104. I can do way better than they are doing.

Real estate tax is property tax and can be found usually by going to the county assessor’s website and attempting to pay the tax for them. It will helpfully show you what is owed for the previous year. You will want to call and find out how values are assessed in the property’s area, so you can estimate better. Beware that sometimes the value will get changed automatically on a sale to the new value. If the price you pay is a lot higher than what the seller paid, you’ll find yourself having a much higher tax bill too. Another way to estimate is by finding the property tax rate, or mill levy, for the area and multiplying that by your final price.

Interestingly, my estimated expenses are quite a bit better than theirs. That’s nice to see and makes me think the deal might actually work after all. For now. But, we aren’t done yet.

The last column is the expense ratio again. It doesn’t care what the individual expenses are. It just assumes that I’ll have to spend 45% of the scheduled rent in expenses. You’ll notice that my expense ratio is 39.2%, which is low for my properties. This tells me that I’ve underestimated something in the expenses and I should look over them again. I’m going to leave it for the purposes of this exercise.

Next time, we will put in financing from the bank. You did talk to your banker by now, didn’t you?